Investor FAQ

What is the tax credit and why is it available?

In 2005, Georgia approved the Film Tax Credit to generate revenue and entice Film Producers to come to the state. In 2008 Georgia passed O.C.G.A. §48-7-.40.26 to further entice game and film production in the state for the purpose of creating jobs and increase expenditures in the state. The production company can sell the credits to raise capital to offset expenses of the production.

Who can buy entertainment credits?

Anyone who has a tax liability to the state of Georgia can purchase and use the entertainment tax credits. This includes individuals, corporations, trusts, partnerships, and LLCs. The tax credits apply to the company’s Georgia tax liability. Should the company have limited or no Georgia tax liability, then the credit may be transferred or sold once to one or multiple Georgia-based taxpayers to use against their tax liabilities.

How do you purchase entertainment credits?

Once you have identified your Georgia income tax liability, you can work with us to enter into an agreement to purchase the credits from the production company. The production company files their tax return with the state along with an IT-FC. We then file the IT-TRANS with the Film Office and the Georgia Department of Revenue providing them with buyer’s name, tax ID information, and amount of credits acquired. The IT-TRANS is provided to the buyers to claim the credit on their Georgia return.

How does this work on my tax return?

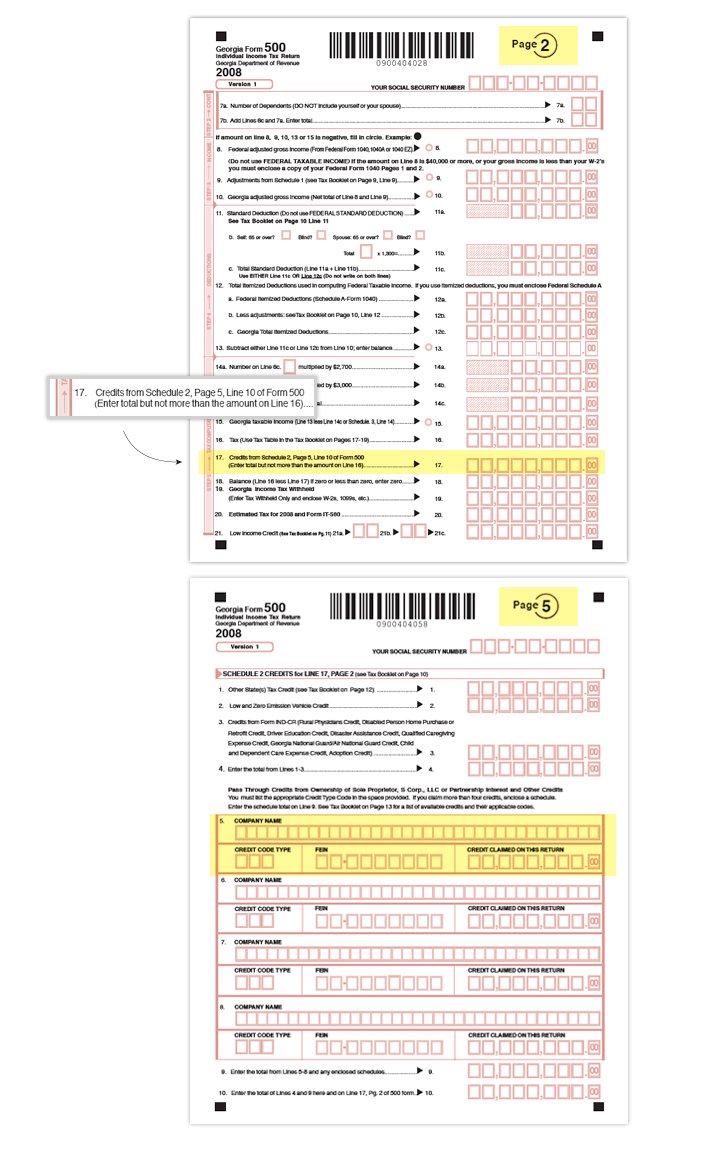

There is nothing that needs to be attached to the return. On page 5 of Georgia Form 500, you will list the name of the Company that you bought the credits from, their Federal ID number, the amount of credits, and use Code 122, which GA has assigned to Film Tax Credit. At closing, you a copy of the fully executed transfer agreement. (The transfer service agreement is between the Company establishing the credit and the purchaser of those credits).

Below is an example of how Individuals will claim credit through the Georgia Tax Form 500. Corporations will use Georgia Form 600. Please contact us for more information about claiming tax credits.

When can I buy and what years of my taxed can I take the credits?

You can buy credits now and apply them in the year purchased or in the year the seller established them, i.e. – tax credits bought in 2012 from a company that generated credits in 2011 can be applied against the 2011 or2012 liability.

What if I buy too many and can’t use all of them for the year I thought I would need them?

Tax credits can be carried forward 5 years from the date in which they were established by the seller (Production Company). For example, tax credits established in calendar 2012 may be carried forward until used or until expiration on December 31, 2017.

Do I have additional risk of an audit?

We have been advised by the State Department of Revenue that no additional risk of audit will apply.

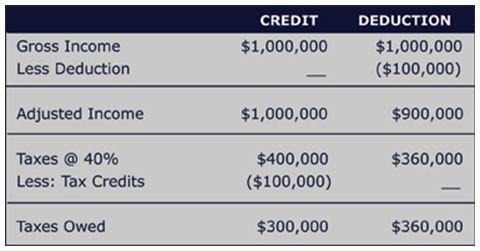

What is the difference between credits and deductions?

Credits are different from deductions in that deductions reduce the amount of income that a taxpayer is taxed upon, while credits offset the taxes directly. $1 of credit reduces $1 of tax liability. $1 of deduction reduces taxable income by $1.

What is the risk?

CSG partners with the most active CPA and auditing firms in the Entertainment tax credit marketplace and these firms are responsible for providing a “comfort letter.” This letter summarizes the tax due diligence procedures that assists in the evaluation of expenditures that qualify for the Georgia Entertainment Industry Investment Act Tax Credits pursuant to O.C.G.A 48-7-40-26. We feel that any recapture is mitigated by taking this extra measure and if any recapture occurs at all it would be extremely small.

What are the highlights of the 2008 Georgia Investment Act?

- Previous multi-part, tier incentive is now 20% flat tax credit on qualified Georgia expenditures.

- The foundation of the Act is a 20% investment tax credit. Production companies that spend a minimum of $500,000 in the state on qualified production and post-production expenditures in a single year are eligible for this credit. This includes most materials, services and labor. The 20% credit applies to both residential and out-of-town hires working in Georgia with a salary cap of $500,000 per person, per production, when the employee is paid by “salary,” which is defined as being paid by W2. If the production company uses a 1099 or a personal services contract to hire someone this limit does not apply.

- Provides an additional 10% tax credit if a production company includes a Georgia promotional logo in the qualified finished feature film, TV series, music video or video game project.

- Provides the same tax credits anywhere in the State of Georgia.

- Provides the same tax credits to all instate and out-of-state labor working in Georgia

- Commercials and music videos are eligible for the 20% base tax credit once the production company has spent a minimum of $500,000 on qualified expenditures during a single year. This may be through a single project or multiple projects.

- The tax credits apply to the company’s Georgia tax liability. Should the company have limited or no Georgia tax liability, then the credit may be transferred or sold once to one or multiple Georgia-based taxpayers to use against their tax liabilities.

- In addition to feature film and television production, the Act also includes other areas of original entertainment content creation including animation, interactive entertainment and video game development.

For more information, please contact:

Joseph Switzer (404) 497-8894 jswitzer@CSGfirst.com